What 30,000+ New Beds Mean for India?

As India continues to advance its healthcare infrastructure, one of the most pressing topics is the availability of hospital beds and the doctor-to-patient ratio across the country. With a population of over 1.4 billion, the demand for accessible, quality healthcare is more important than ever.

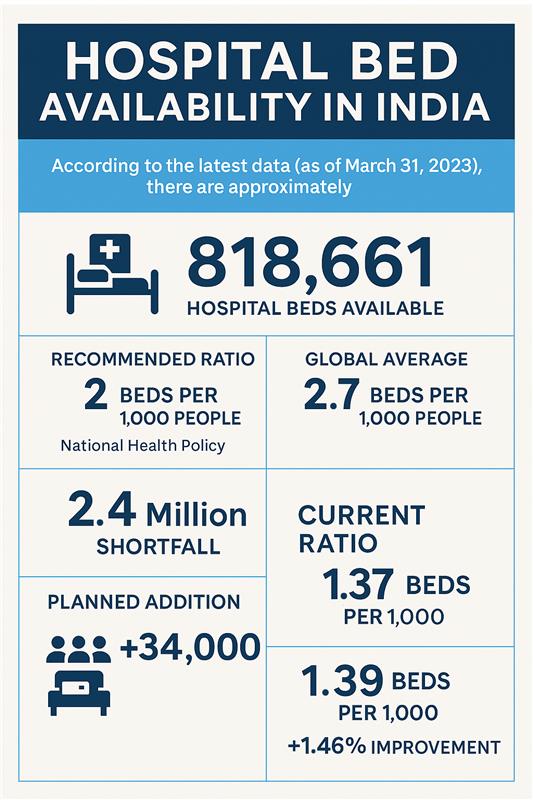

The Current State of Hospital Bed Availability

According to the latest data (as of March 31, 2023), there are approximately 818,661 hospital beds available in the country. This figure reflects the collective capacity of public and private healthcare institutions.

The National Health Policy recommends a ratio of 2 beds per 1,000 population, while the global average stands at 2.7. Estimates from the private sector suggest that there could be as many as 1.18 million beds in total. Even so, based on current healthcare needs and population trends, India faces a shortfall of nearly 2.4 million beds.

According to a recent joint analysis published by Knight Frank and Berkadia, India's current bed-to-population ratio is 1.37 per 1,000. In perspective, with the planned addition of 30,000+ new beds, the total would rise to 2,032,661, nudging the ratio up to 1.39 per 1,000—a 1.46% improvement. While modest, this increase signals a step in the right direction toward narrowing the healthcare gap.

Regional Developments

The addition of 30,000+ new hospital beds across India is a step forward in addressing the existing healthcare infrastructure gap. These beds are being distributed across different regions based on current availability and projected population needs.

- North India will see the highest allocation with 15,640 new beds, bringing the total in the region to approximately 585,640 beds. With an estimated population of 50 crore, this increases the bed-to-population ratio from 1.14 to 1.17 per 1,000 people, a 2.6% improvement. While still below the recommended standard, it indicates progress in closing the gap.

- South India will receive 10,200 additional beds, raising its total to around 580,200 beds for a population of 45 crore. The region currently outperforms others, and the new additions will boost the ratio from 1.27 to 1.29 per 1,000, or a 1.6% rise.

- Western India is expected to add 4,420 beds, increasing the total to about 384,420 beds. For its population of 40 crore, this results in a minor shift from 0.95 to 0.96 beds per 1,000, a 1.1% growth. Though the improvement is modest, it adds capacity in an area with growing urban populations.

- Eastern and Central India together will get 3,740 new beds, raising the combined total to 383,740 beds for a population of approximately 55 crore. This changes the region’s ratio from 0.69 to 0.70 per 1,000, a 1.4% increase. While the numbers remain below national averages, the development could begin to ease some of the existing strain.

These regional shifts, though incremental, reflect an attempt to distribute resources more equitably. The improvements are modest but necessary, especially in areas with historically lower healthcare infrastructure. However, much more will be needed to meet the national goal of 2 beds per 1,000 people, let alone the global average of 2.7.

The doctor-to-patient ratio is better than average. But with caveats

India currently boasts a doctor-to-patient ratio of 1:834, which meets and even surpasses the WHO-recommended minimum of 1:1,000. This figure includes all registered doctors across AYUSH and allopathy practices. When considering only allopathic doctors, the ratio is closer to 0.92 per 1,000, revealing some room for improvement, especially in rural regions.

Comparing globally, countries like Austria (5.5 doctors per 1,000), Germany (4.1), and France (3.2) highlight how far India can still go in strengthening its healthcare workforce.

There is a significant disparity in doctor density between urban and rural areas. With urban areas typically having a higher ratio. The rural regions exhibit a concerning doctor-to-patient ratio of approximately 1:25,000, significantly below the WHO recommended ratio of 1:1000, highlighting the importance of deliberate resource allocation and incentives for medical professionals to practice in less populous areas.

What This Means for Smaller Hospitals

The planned addition of 30,000+ hospital beds especially in Tier 2 and Tier 3 cities has the potential to reduce the overwhelming patient load currently seen in urban hospitals. This decentralization of care may help alleviate pressure on overburdened metro facilities and improve access for patients closer to their communities.

However, the expansion also introduces new dynamics for smaller and mid-sized hospitals.

As larger hospital chains with advanced technology and infrastructure enter these markets, the competitive landscape will evolve. Smaller hospitals may feel increased pressure to adopt new practices, improve service quality, or upgrade their infrastructure to keep pace. In some cases, the influx of new beds and providers could lead to greater competition in the healthcare market, potentially driving down prices and squeezing profit margins, particularly for standalone or resource-constrained institutions.

This environment may also encourage consolidation, as some smaller hospitals could face pressure to merge with or be acquired by larger players in order to remain viable. If they are unable to adapt to the changing expectations of patients and the broader ecosystem, sustaining independent operations may become more challenging.

Additionally, large hospital chains are likely to attract more patient footfall due to their brand visibility, technological edge, and comprehensive range of services. This could result in reduced patient inflow and revenue for smaller hospitals unless they carve out a niche or differentiate effectively.

That said, this shift also opens up opportunities. Smaller hospitals that focus on specialized services, personalized care, or underserved segments may be well-positioned to thrive even amidst intensified competition.

Employment Outlook: A Ripple Effect

As new beds are added and infrastructure expands, so will the demand for skilled professionals, from doctors and nurses to technicians and support staff. Construction and maintenance work will also see a boost, offering temporary job creation during the setup phase.

This healthcare expansion may catalyze employment growth in tier 2 and tier 3 cities, creating a ripple effect across ancillary industries such as logistics, pharmaceuticals, medical equipment, and digital health services. However, it will also likely lead to greater competition for skilled talent, pushing hospitals to prioritize effective recruitment and retention strategies.

The Patient Perspective

Expanding bed capacity is likely to reshape the healthcare landscape. In positive terms, it will increase access to healthcare, particularly in underserved districts. For patients, the addition of hospital beds can translate to shorter wait times, timelier admissions, and improved quality of care. It also presents the potential for more localized treatment options, reducing the need for long-distance travel for procedures and emergencies.

A Collective Effort

Reaching the ideal benchmark of 7 beds per 1,000 population, as suggested by Dr Kiran Madhala, Secretary General of Telangana teaching government doctor association, will require long-term planning, public-private partnerships, and sustained investment. While the addition of 30,000+ beds may seem small in the broader context, it is a constructive move toward a more inclusive, better-equipped healthcare system.

India’s healthcare journey is one of steady progress, not an overnight transformation. The key lies in building capacity while ensuring equity, strengthening the workforce, and empowering both large and small players in the healthcare ecosystem.